Financial Review

Toshimi Sato

Representative Director

Executive Vice President

FY2022 Review and Outlook for FY2023 Business Environment

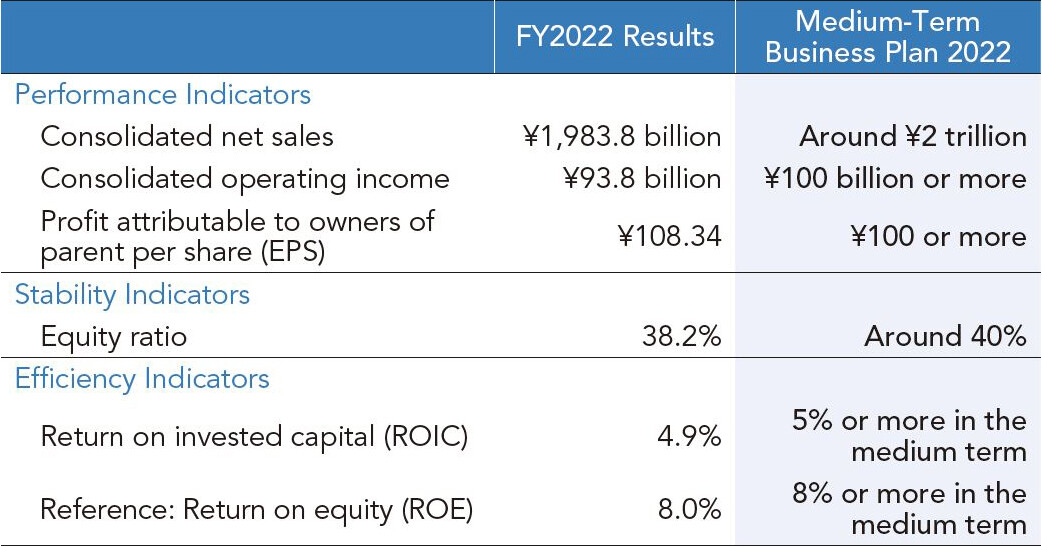

In March 2022, the Obayashi Group formulated Medium-Term Business Plan 2022. The plan declared the Group's intention to secure stable earnings, and set securing a minimum of ¥100 billion in consolidated operating income as one of the performance targets for the five years from FY2022 to FY2026. In FY2022, the first year of the plan, consolidated operating income fell short of that target at ¥93.8 billion. However, we did achieve our targets for earnings per share (EPS), equity ratio, and return on invested capital (ROIC), which was newly adopted as a management indicator for Medium-Term Business Plan 2022.

The environment facing the Japanese economy has changed dramatically since the current medium-term plan was drawn up. In fact, we have seen raw materials and energy prices soar due to the Russia-Ukraine situation and other factors, as well as disruption in global supply chains, and rising import prices caused by the rapid depreciation of the Japanese yen. We are also witnessing unprecedented price increases on a wide range of materials in the construction market. The projects for the Obayashi Group that have been most affected by these developments are those in the domestic construction business for which we obtained priority negotiation rights in bids conducted up to FY2021, and this is one of the reasons why the Group's FY2022 performance came in lower than originally anticipated.

Medium-Term Business Plan 2022: Performance Indicators and Targets

Results of the domestic construction business are expected to be even more severely impacted in FY2023 than in FY2022 for several reasons. The prices of raw materials for construction are expected to remain high. Significant progress is being made on the construction of several large-scale properties for which we recorded provisions for loss on construction contracts, but those projects are not contributing to profits. Finally, labor costs for skilled workers are expected to increase and, at this point in time, there is little prospect of an improvement in profits from civil engineering construction projects in hand either. We are, however, currently taking steps in the domestic construction business such as reviewing contract terms to address material price rises, so we expect earnings will improve toward the latter half of the current medium-term plan.

Domestic construction demand is holding steady and we expect construction demand to increase in multiple manufacturing fields, including semiconductors, storage batteries, machine tools, general machinery, and electrical machinery, as production bases are brought back to Japan and the government designates more commodities as specific critical products. We also expect capital expenditure for electric vehicle (EV)-related facilities and for data centers to rise as decarbonization and digitalization efforts pick up speed. In non-manufacturing sectors, we expect to see continued demand for large-scale urban redevelopment projects and the building of distribution facilities. In the civil engineering field, we foresee continued long-term demand for expressways and other infrastructure development, including repairs and renewal, and we expect construction demand to increase as the government strives to build national resilience and promote renewable energy policies.

In our overseas business, construction investment has been recovering in Asia as economies start to recover from the COVID-19 pandemic, while uncertainty surrounding construction investment in the office market and other non-manufacturing sectors persists in North America due in part to monetary policies and the performance slowdown of GAFAM,(*1) and other factors.

- *1 The acronym for Google, Amazon, Facebook (currently Meta), Apple, and Microsoft, which are major technology companies in the U.S.A.

Pursuing ROIC Management

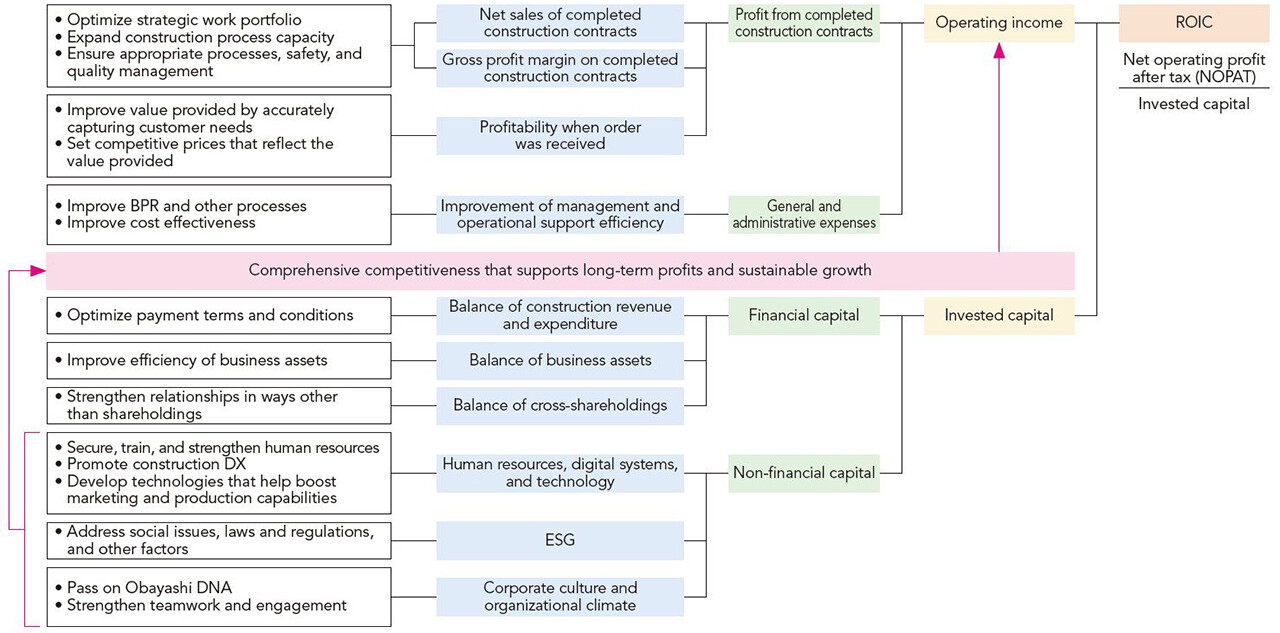

We need to address performance in various parameters in order to ensure sustainable development for the Group. Naturally, we must seek to improve the value we offer customers and to improve profitability while maintaining a firm commitment to safety and quality. However, we also need to improve capital efficiency by enhancing our management resources and conducting optimal investment in order to secure a level of earnings that exceeds the cost of capital. With that in mind, we adopted return on invested capital (ROIC) as one of performance indicators in Medium-Term Business Plan 2022, and set a minimum ROIC target of 5% or more over the medium term based on the cost of capital for the Group. In the previous plan (Medium-Term Business Plan 2017), we used return on equity (ROE) as a performance indicator. However, we decided to review the performance indicators because we wanted to evaluate the efficiency not only of equity but also of overall invested capital. We also wanted to further optimize working capital and improve the effectiveness of our investments, and at the same time ensure solid investment in intangible assets, such as human resources, digital systems, and technology, which we believe will strengthen our competitiveness in the future.

To improve ROIC for the entire Group, we must maximize and efficiently utilize management resources and improve individual ROIC in each of the Group's businesses from domestic construction, our core business, to the overseas construction business in North America and Asia, real estate development business, and green energy business. Given the different risks for each business and varying expected yields in each market, we intend to make clear the weighted average cost of capital (WACC) level for, and evaluate the significance of, each business. The Obayashi Group will strive to increase its corporate value by strengthening its business portfolio based on the WACC and the target ROIC level for each core business.

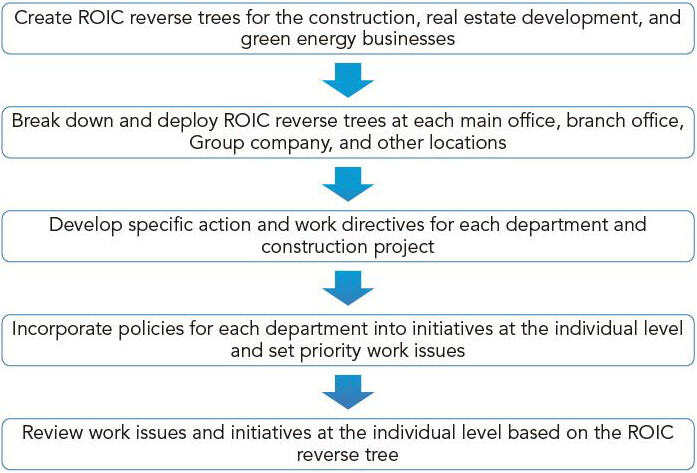

We use the ROIC reverse tree to help people within the Company understand and pursue ROIC management and work to improve productivity through operational reforms. Instilling ROIC management in the construction business, for example, doesn't just involve the pursuit of measures to improve profits on completed construction projects and reduce general and administrative expenses in order to generate higher operating income, but also involves considering the need to optimize financial capital and invest in non-financial capital. In FY2022, we launched ROIC reverse trees for the construction, real estate development, and green energy businesses that are tailored to the specific business characteristics of each main office, branch office, and domestic and overseas Group companies. We then took into account specific actions in each department and construction project as well as any issues and initiatives at the individual level and reviewed the status of implementation at the end of the fiscal year. We will continue to promote investment in important management resources such as human resources and technology, which support the sustainable growth of the Group. We will also continue to use the ROIC reverse tree to promote operational reforms that will help improve ROIC.

Deployment of ROIC Reverse Tree Method

Example ROIC Reverse Tree for the Construction Business

Investment Progress under Medium-Term Business Plan 2022

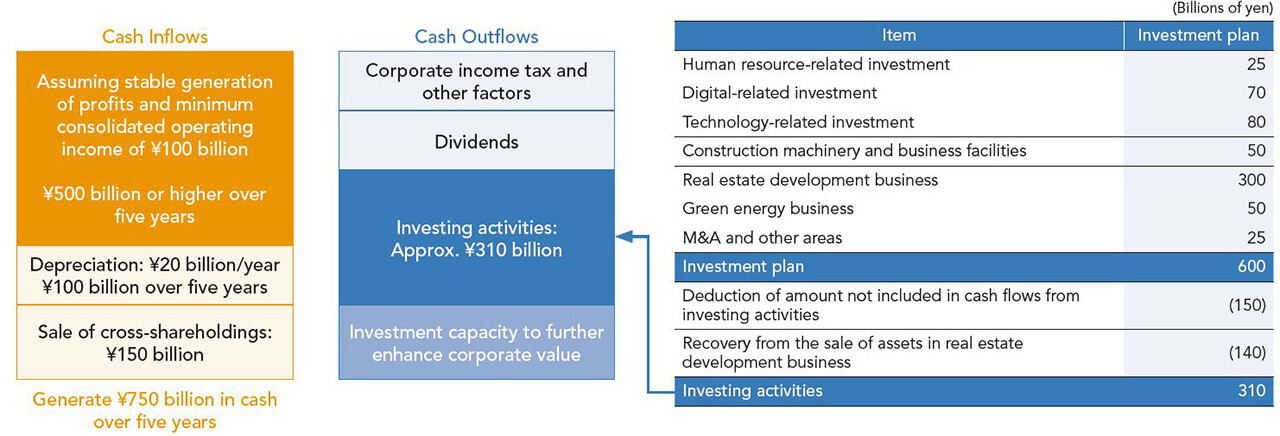

Regarding cash allocations in Medium-Term Business Plan 2022, we use cash inflows from business income based on performance targets, the sale of cross-shareholdings, and other items as our source of funds. We plan our cash outflows after thoroughly considering the balance between the following three elements:

- The scale of equity capital required to ensure corporate stability in an uncertain era

- The amount of growth investment required to maintain a company's competitive advantage and further enhance its corporate value

- Stable shareholder returns over the medium to long term

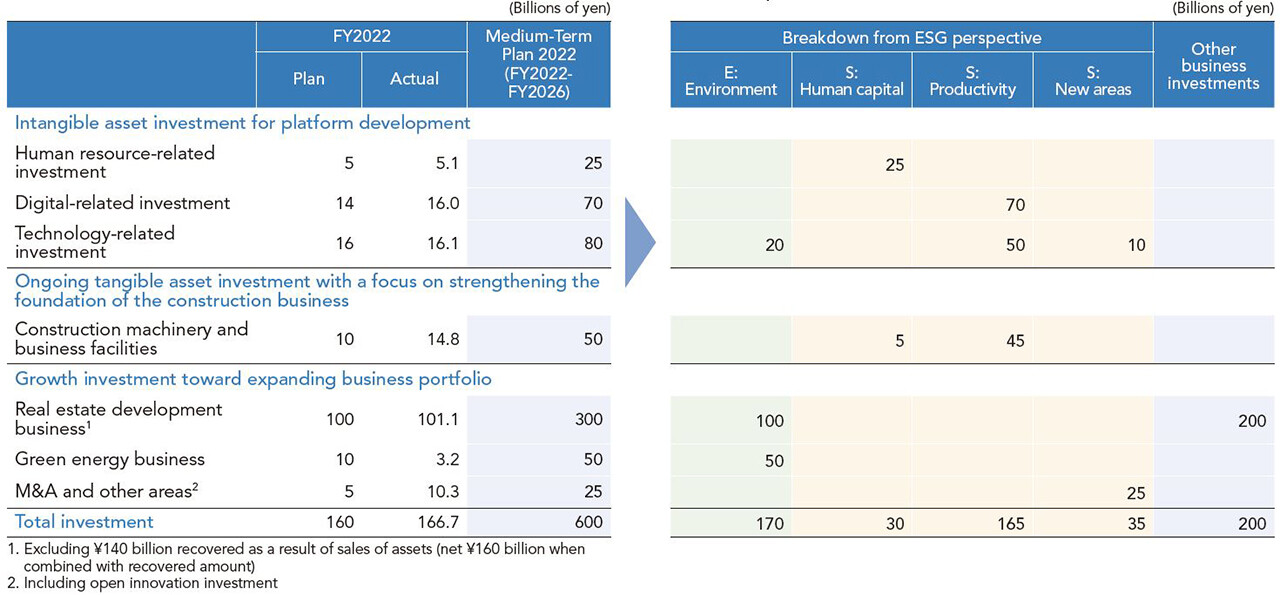

We plan to invest a total of ¥600 billion to improve corporate value over the five years of Medium-Term Business Plan 2022, and we invested ¥166.7 billion toward that end in FY2022, the first year of the plan. With regard to human resource-related investment, we formulated the Obayashi Group Human Resource Management Policy in December 2022, and we are now working to expand our training systems, develop personnel systems that facilitate diverse work styles, secure and train human resources, and improve employee engagement. Regarding investment in digital systems, technology, construction machinery and business facilities, and other relevant areas, we are implementing investments designed to improve productivity in anticipation of the application of regulations to cap overtime work in the revised Labor Standards Act of Japan from FY2024. In the real estate development business, we are looking to diversify asset types by expanding the scope of our business from offices to distribution and other facilities, and to globalize our business portfolio by developing and acquiring properties in London and developing properties in Thailand. We are also using the private fund established by the Group to refresh our asset portfolio and improve the efficiency and profitability of our investments. On the M&A front, we formed a capital alliance with timber manufacturer and distributor Cypress Sunadaya Co., Ltd. This alliance is designed to help strengthen supply chains in the construction market for non-residential wooden structures and timber interiors, an issue that the Group needs to address in promoting the Circular Timber Construction® recycling-oriented business model.

The Medium-Term Business Plan 2022 Cash Allocation

Breakdown of Cash Flows from Investing Activities

Investment Plan for Medium-Term Business Plan 2022 (FY2022 to FY2026)

Breakdown of ¥600 Billion Investment from ESG Perspective

Reducing Cross-Shareholdings

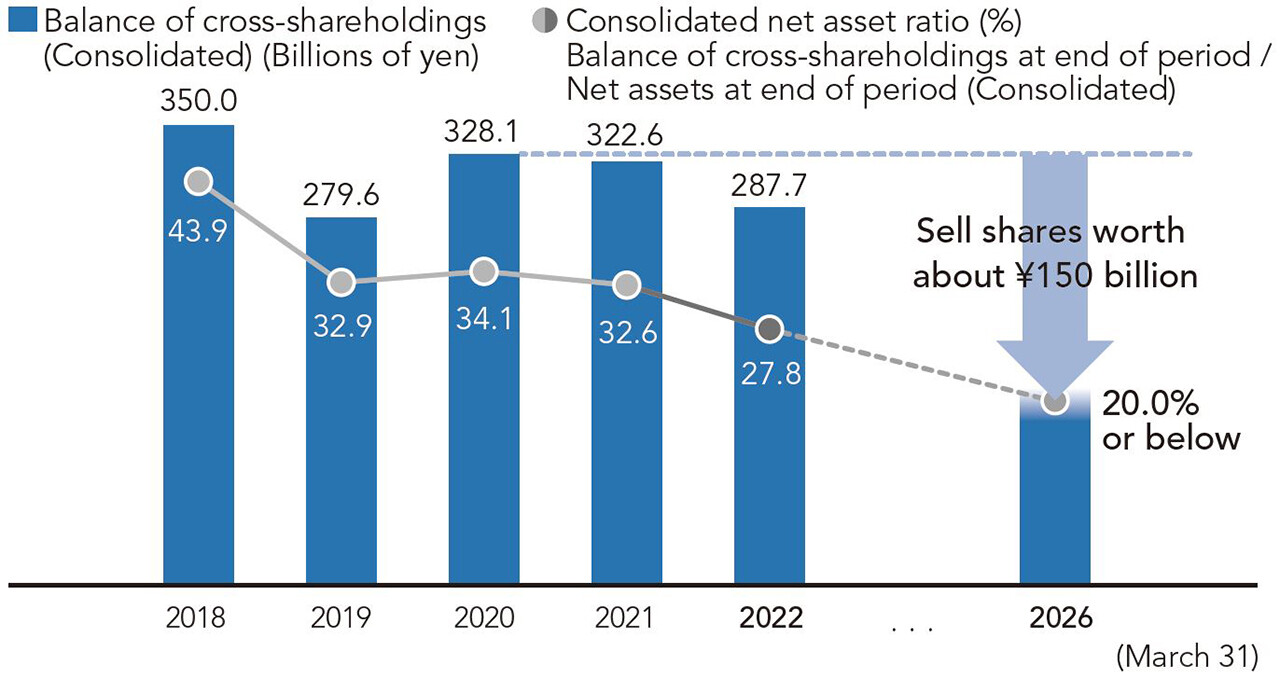

Obayashi Corporation holds shares in customers' businesses (hereinafter, "cross-shareholdings") for the purpose of maintaining and strengthening business relationships. We consistently verify the medium- to long-term economic rationale of these crosss-shareholdings and sell holdings whose significance has diminished from a business perspective based on a comprehensive consideration of capital costs, business returns, and valuation risks. We use the cash generated from the sale of cross-shareholdings to increase corporate value by effectively investing in vehicles that offer stable income and in areas that contribute to sustainable growth.

We instigated a further review of the significance and efficiency of cross-shareholding investments as part of Medium-Term Business Plan 2022. We committed to selling a total of around ¥150 billion in cross-shareholdings, starting in FY2021, to reduce cross-shareholdings to 20% or less of consolidated net assets as soon as possible before the end of March 2027. We sold a cumulative ¥41.5 billion in cross-shareholdings on a consolidated and market price basis over FY2021 and FY2022, which represents 27.7% of the targeted sales amount. As of the end of March 2023, the value of cross-shareholdings totaled ¥287.7 billion, or 27.8% of consolidated net assets. If we include cross-shareholdings that we have already agreed to sell, cumulative sales of cross-shareholdings would be ¥56.3 billion, or 37.5% of targeted sales.

Achieving the targeted cross-shareholding sales requires the understanding of the business partners that we hold shares in, so we will continue to participate in careful dialogue to carry out those sales.

Changes in Balance of Cross-Shareholdings and Consolidated Net Asset Ratio

Changes in Sale of Cross-Shareholdings

Cumulative Amount Sold from FY2021 (Progress Rate vis-à-vis the Target of ¥150 BIllion)

Shareholder Returns

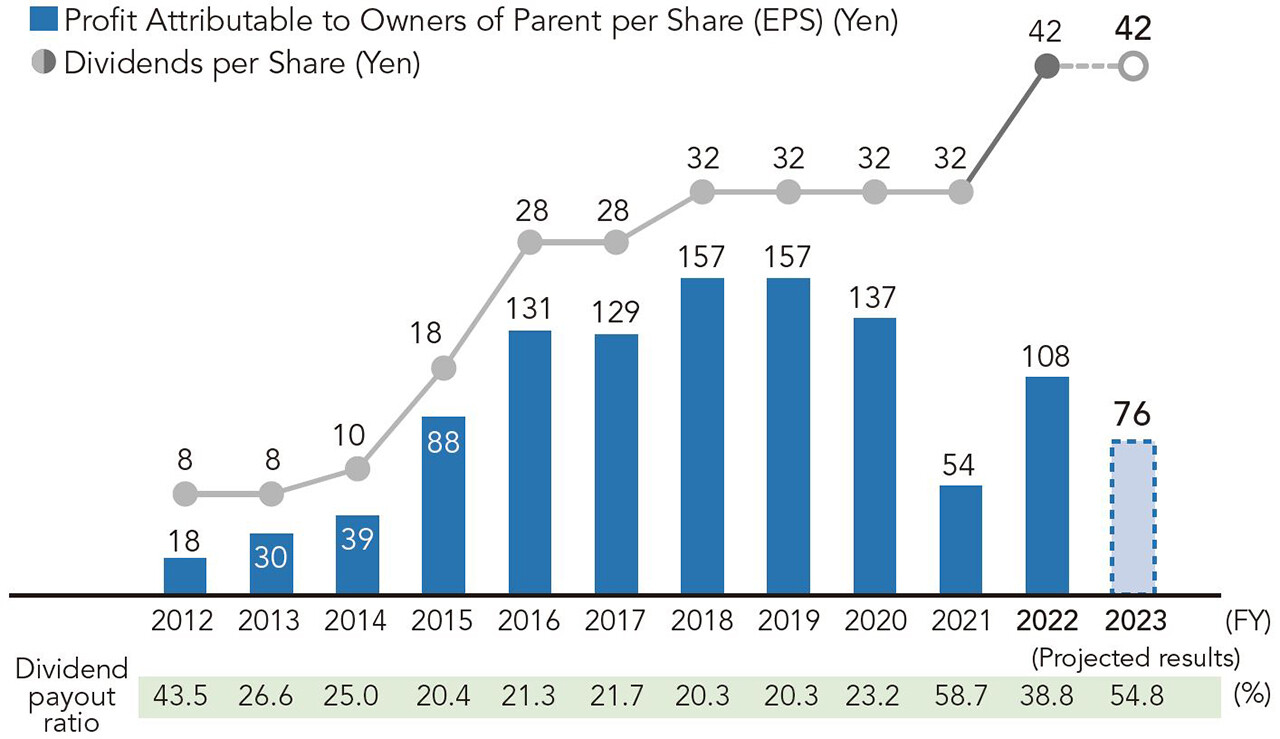

We stipulated a dividend policy in Medium-Term Business Plan 2022 that involved achieving a dividend on equity (DOE) ratio of approximately 3%. Maintaining stable long-term dividends is a top priority. With that priority in mind, we stipulated the policy to provide stable shareholder returns over the medium to long term by using profits accumulated primarily during Medium-Term Business Plan 2017 to enhance equity capital. That policy also considers the business plan and the growth investment strategy for increasing corporate value for the five-year term of Medium-Term Business Plan 2022. Based on that policy, we increased the annual dividend for FY2022 by ¥10 year on year to ¥42 per share. The Company is committed to strengthening its earnings base through growth investments and efforts to increase corporate value over the medium-to long-term, while also providing shareholders with stable dividends based on DOE to appropriately reflect equity levels.

However, given the significant changes in the business environment envisaged in the current medium-term plan, we believe it is necessary to restate the Group's growth strategy and planned steps for improving corporate value. As part of that effort, we will explore the best capital policy, which would include the consideration of various options, such as dividend increases and share buy-backs, taking into account market requests relating to the price-to-book ratio (PBR) of our shares.

Earnings Per Share (EPS) and Dividend Per Share

Improving Corporate Value

Through Medium-Term Business Plan 2022, the Obayashi Group will contribute to creating a sustainable society according to its vision for 2050 and the Obayashi Philosophy. To that end, the Obayashi Group strives to strengthen its business foundation and accelerate Company-wide transformation based on three fundamental strategies: (1) strengthen and expand the foundation of the construction business, (2) innovate technologies and businesses, and (3) expand the business portfolio for sustainable growth. The entire Group is getting behind the effort to view the dramatic changes in our business environment as a growth opportunity, as we seek to respond flexibly and decisively to change, work tirelessly to strengthen our management foundation, and strive to increase corporate value through continuous growth.

IMPORTANT NOTICE

U.S. Disclaimer - Unsponsored ADR (American Depository Receipt)

Effective October 10, 2008, the United States Securities and Exchange Commission (SEC) made it possible for depository institutions or banks to establish ADR programs without the participation of a non-U.S. issuer (a so called "Unsponsored ADR")." An ADR, or American Depositary Receipt, is a negotiable receipt, similar to a stock certificate, which is issued by a U.S. bank or depository to evidence an ordinary share of a non-U.S. issuer that has been deposited with the U.S. bank or depository. ADRs permit a U.S. investor to purchase in a U.S. market an interest in a non-U.S. issuer's securities. An ADR program which is unsponsored is set up without the non-U.S. issuer's cooperation or even its consent. Obayashi Corporation (hereinafter the "Company") does not support or encourage the creation of unsponsored ADR facilities in respect of its securities and in any event disclaims any liability in connection with an unsponsored ADR. The Company does not represent to any depository institution, bank or anyone nor should any such entity rely on a belief that the Web site of the Company includes all published information in English, currently, and on an ongoing basis, required to claim an exemption under U.S.Exchange Act Rule 12g3-2(b).

DISCLAIMER

The information posted on Obayashi Corporation's English website was translated from Japanese into English and presented solely for the convenience of non-Japanese speaking users. The purpose of the English information provided herein is to provide the stakeholders of Obayashi Corporation with its financial and non-financial information for their better understanding of Obayashi Corporation and its group companies, and is not to solicit any person or entity to buy or sell Obayashi Corporation's securities of any kind. If there is any discrepancy between original Japanese information and its English translation, the former will prevail. Any statements made about Obayashi Corporation's future plans, forecasts, strategies and performances are forward-looking statements subject to risks and uncertainties. Forward-looking statements included herein are made based on the information available at the time of the release of the statements. Due to various factors, actual result may vary from what was anticipated in the forward-looking statements.